The experience of paying for products and services online is set to undergo significant changes in the coming years.

Starting in 2030, Mastercard will eliminate the need for Europeans to manually enter their card numbers when checking out online, regardless of the platform or device they use.

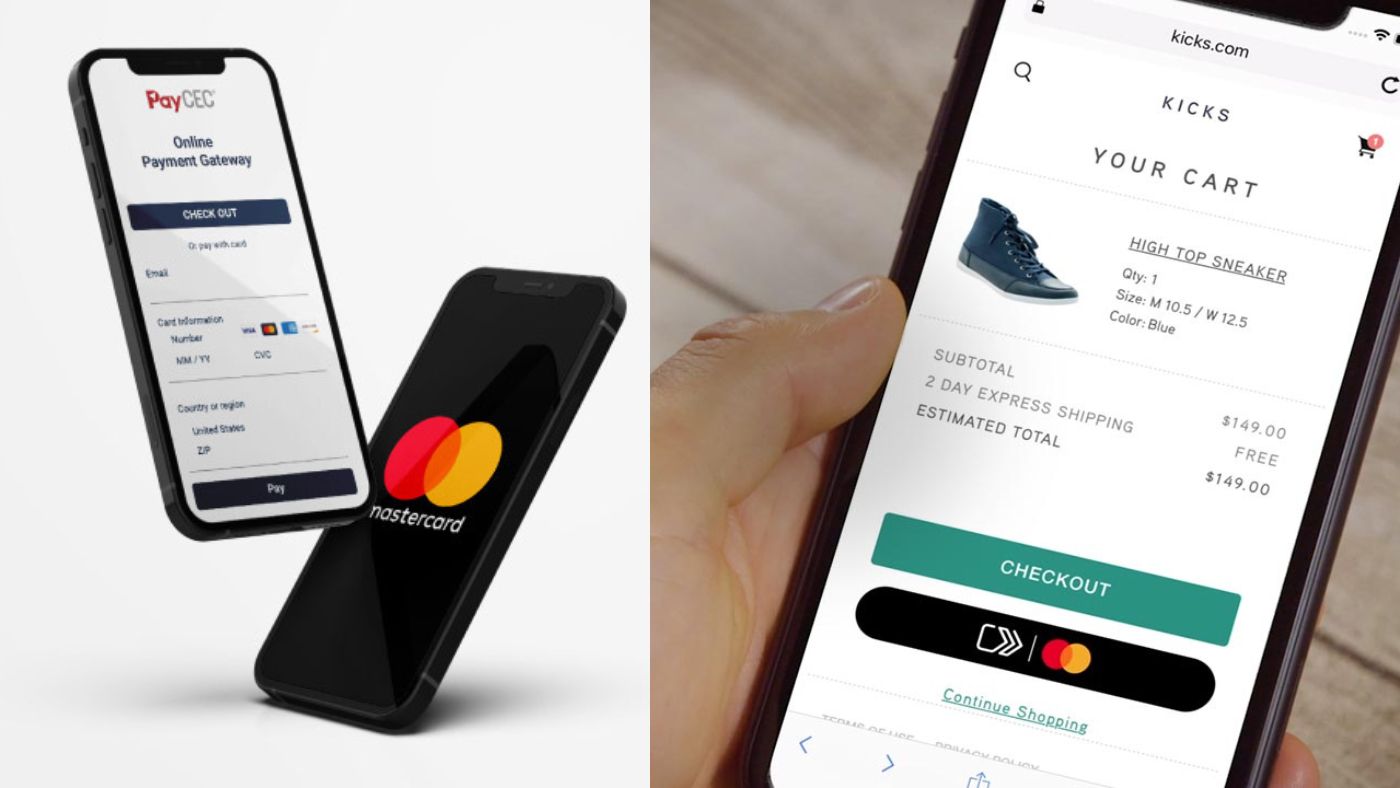

Mastercard will announce that by 2030, all cards issued on its network in Europe will be tokenized.

This means that instead of the traditional 16-digit card number, transactions will use a randomly-generated “token.”

Mastercard has been collaborating with banks, fintechs, merchants, and other partners to phase out manual card entry for e-commerce by 2030 in Europe, replacing it with a one-click button across all online platforms.

This shift aims to enhance security against fraud attempts, according to Mastercard.

Users will no longer need to enter passwords for each payment, as Mastercard introduces passkeys to replace passwords.

Additionally, customers will be able to make one-click payments at checkout using biometric authentication, such as a thumbprint.

Cards stored on a merchant’s page or in an electronic wallet via tokenization can be automatically updated whenever they are replaced or renewed.

Mastercard claims that achieving 100% tokenization across e-commerce sites will significantly reduce fraud rates.

Market research firm Juniper Research projects that losses from online payment fraud will exceed $91 billion by 2028, totaling more than $362 billion globally over the next five years.

Mastercard notes that the adoption of tokenization has been increasing at a rate of 50% annually and now secures about 25% of all e-commerce transactions globally on its network.

The change is being rolled out in Europe, a leader in payment innovations like contactless payments and online banking, which allowed users to share account data to access new financial products.

“In Europe, we have seen tokenization gaining momentum across the ecosystem; the convenience and reduced rates of fraud sell themselves,” said Valerie Nowak, executive vice president, product and innovation at Mastercard Europe.

“We are confident that reaching this vision by 2030 is a win-win-win for shoppers, retailers, and card issuers alike.”

From the introduction of credit cards in the 1950s and 1960s to the online payment shift with the internet’s rise in the early 2000s, payment methods have undergone significant transformations.

Initially, bank clerks checked card numbers against a list of invalid numbers or called the issuing bank to verify identities.

“Zip-zap” machines imprinted card numbers on carbon paper packets until the 1970s and 1980s when magnetic stripes and electronic payment terminals became prevalent.

These were later succeeded by microchip cards storing data on the cardholder, card number, and expiry date.

Mastercard anticipates that this move toward an “embedded” payment system will be as impactful as the adoption of chip and PIN or contactless payments, which are now widespread in developed economies.

The company asserts that its technology will make online payments as seamless as contactless payments in stores, enabling consumers to make one-click payments across various devices, including smartwatches, home assistants, and even cars.

For instance, Mastercard has a partnership with Mercedes-Benz that allows the automaker’s customers to use a fingerprint sensor in their cars to make digital payments at over 3,600 service stations across Germany.